It is the art and science of making decisions about investment mix and policy, matching investments to objectives, asset allocation for individuals and institutions, and balancing risk against performance.

Portfolio management is all about strengths, weaknesses, opportunities and threats in chosing an adequate mix of Insurances and Investments.

Insurance Portfolio Management

Insurance in India is the most lighly taken thought by Individuals and Corporates. Most Insurance Plans are bought without considering the real requirements and knowing facts. Bluntly saying, it is more of an Obligation Purchase, Reference Purchase, Bank / Legal / Contractual Binding or a Tax Saving tool.

Resultingly, one gather a large bunch of Insurance Policies with actually no idea of what they are. Moreover, under the psychological burden of carrying sooo many policies, one doesn't even think of his shortfalls and restructuring in the absence of time, knowledge and money.

Insurance Portfolio Management consists of the following steps:

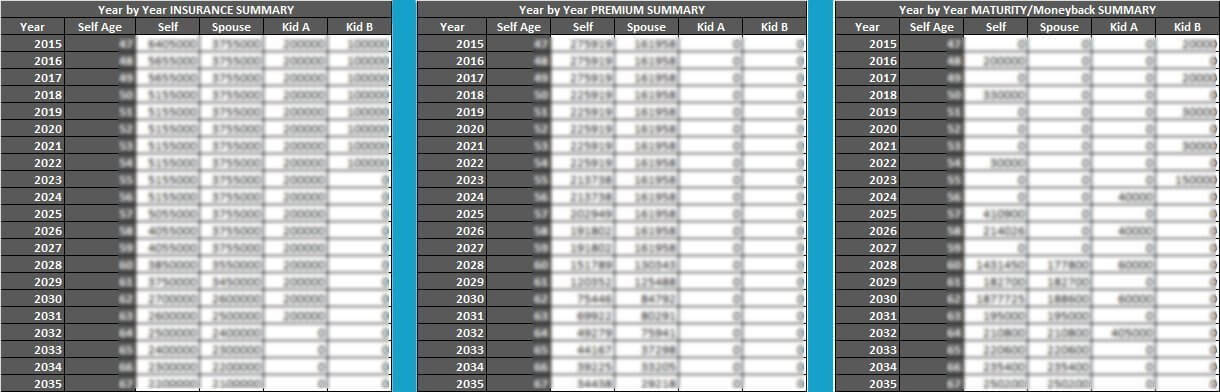

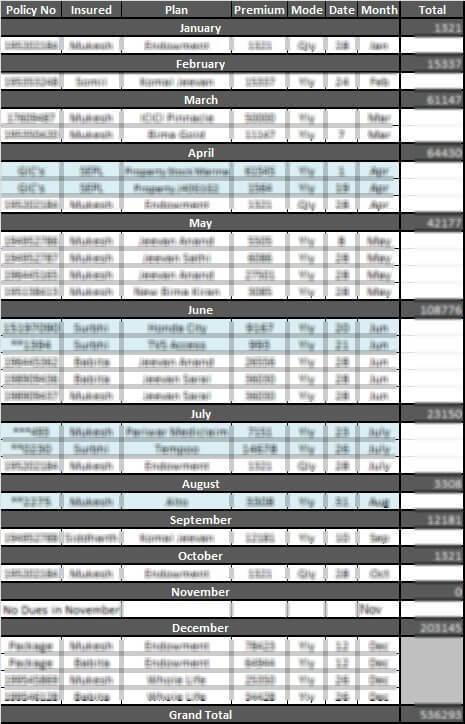

The final product somehow looks like this:

Insurances

Summary

Premium Calender

Investment Portfolio Management.

In the dynamic financial market, it is really very difficult to keep a track of your Investments. Investments are often done in the lack of knowledge & time. Moreover, the availability & approach of part time financial consultants makes it worse to manage. You keep on looking for statements, notices, matured deposits, unclaimed dividends, difference in signatures, un-noticed investments, profit folios, loss folios and lot more..

We, at Meri Planning help you Track your investments in a better way. We provide online platforms for investment in Mutual Funds enabling you to overcome your investment related issues with a single click.

You can >>

'Simplify the Complicacies' is what we deal in. So let's understand some basic Jargons of Life Insurance

Also called "Pure Insurance", Term Insurance provides a "High Life Insurance Coverage" for a "Specified Tenor" in a "Very Low Premium".

Term Insurance usually doesn't pay any Maturity. It is the Simplest form of Insurance with only 3 things, Sum Insured, Annual Premium and Policy Tenor.

There are also some Term Insurance which Returns all the Premiums paid on Maturity. However, they charge a higher Premium as compared.

These are the simplest and oldest form of Life Insurances. The premium you pay are invested in non-equity instruments like bonds and Long Term Deposits. Thus, they carry lower risk and volatility.

They generally declare yearly dividends also called 'Bonuses' which are mostly floating. Most of these are loanable, however bear high pre-surrender charges.

ULIP is a product that unlike a Term insurance policy gives investors the benefits of both insurance and investment under a single integrated plan. A part of the premium paid is utilized to provide insurance cover while the remaining portion is invested in various equity and debt schemes. Just the way it is for mutual funds, ULIP's also allot units & each unit has a Net Asset Value (NAV) that is declared on a daily basis

Generally Nothing is Guaranteed Except the Death Cover. They are Subject to Market Risks and bear various charges.

Section 80C entitles the assesse to claim Deduction for certain Investments and Expenditure up-to Rs 1.5lacs per year. Life Insurance acquires a major space of 80C in India. For 80C deduction, the Insured Sum should at-least be 10 times of the annual premium paid.

Section 10(10D) exempts income received from a Life Insurance Policy from Tax. Exceptions are: Pension/Annuity plans, Employer Sponsored group life insurance, policy which violates the conditions of section 80C.

Life Insurance is a Contract between the Insurer and Insured. The basis of each contract is Utmost Good Faith. Thus both, insurer & insured shouldn't hide anything material for the insurance contract.

The Insured should not hide any medical ailment, lifestyle habits, heredity issues and Financial eligibility to ensure Claim Settlement. A declaration may invite extra premiums or proposal rejection, but will ensure 100% honor of contract.

An Insurance Company deploys many physical & human resources to manage it's clients. All those expenses are distributed proportionately amongst their clients.

They include Policy Administration Charge, Fund Management Charge, Policy Servicing Charges, Surrender Charges, Mortality Charges and Upfront Charges. Customer should study the charges before taking a policy

In India, a big chunk of life insurance is bought in obligation, lack of knowledge or for tax saving. However, it mostly leads to dis-satisfaction.

A customer should take time to hire a professional to Assemble, Analyze and Restructure their existing policies to suit their needs. Restructuring may require Pre-Close, Switch, Premium Holidays, Additional Purchase and lot. But it leaves you with a light head and clear understanding of where you are!!

'Simplify the Complicacies' is what we deal in. So let's understand some basic Jargons of Health Insurance

A plan where the Entire Family is Covered in a Single Policy and people covered SHARE the total health insurance available to them is called a Family Floater. Thus, the overall claim limit of both, an Individual & the entire family is the same.

Family may contain Self, Spouse, Children and in Some Cases Parents and Other Relatives too. Here, the premiums are generally charged as per the age of the eldest insured.

When instead of an Individual or a Family, the entire Organization or a Formal Group forms a contract with an insurer, it is called a Group Insurance. It comprises of Group Health and Group Personal Accidental Insurance. It has many advantages over Individual insurance.

Benefits: Lower Premiums, High Customization, No pre-policy health checkups required, Higher age of Entry, Addition Deletion in between, Smoother Claims Settlement.

Before buying a Health Insurance Policy, one must closely notice these.

Waiting Periods: Many illnesses are out of scope of the policy for initial 30days, 1/ 2/ 4 years. These mostly comprises of treatments of pre-existing illnesses, cataract, piles, hernia, stone, joint replacement, cyst, sinus and few other surgeries.

Exclusions: There is a set of common & permanent exclusions like War, breach of law, substance abuse, dental treatment, HIV etc.

Cashless: All Insurance Co's have associations with many hospitals, a list of which is provided along with the Policy. If an insured is advised to take a treatment (within the scope of the policy) in these hospitals, they can be treated without paying cash to the hospital. The hospital raises the bill to insurance comp. which approves the allowable amount and pays directly to the hospital.

Reimbursement: Treatments taken in non-network hospitals have to be initially paid by the client. Thereafter, insured may raise all bills, prescriptions, receipts, investigations along with claim for the settlement directly to his bank account.

TPA is an organization that processes claims and performs other administrative services in accordance with a service contract with the Insurance Company. More specifically, a TPA is neither the insurer (provider) nor the insured (employees or plan participants), but handles the administration of the plan including processing, adjudication, and negotiation of claims, record-keeping, and maintenance of the plan. These are intermediaries between the Customer, Hospital and Insurer.

Click to QueryAs per the terms & conditions of the insurance policy, a customer may require to bear a certain percentage of a claim. This Sharing of claims between the Insured and Insurer is called Co-Pay.

In India, Co-pay is generally associated with Client's Age, Specific Illnesses or Hospital Agreement.

A Health Insurance policy mostly requires 24 hours continuous hospitalization for a claim. However their are certain conditions where a patient is eligible for a claim despite getting discharged within 24 hours of admission.

Those treatments taken in-patient in a hospital where due to technological advancement, the treatment can be done within 24 hours are day-care treatments like Cataract, chemotherapy, Cyst Surgeries, Sinus Surgeries and many more..

'Simplify the Complicacies' is what we deal in. So let's understand some basic Jargons of Mutual Funds

A mutual fund is a type of professionally managed investment fund that pools money from many investors to purchase securities. Managed by Professional Fund Managers, they aim to achieve common goals of investors by investing within the Regulations Specified.

They invest in Equities, Debt, Money Market Instruments, Bonds, Specified Commodities & many more.

Units: Just as shares represent the extent of equity ownership in a company, units represent your extent of ownership in a mutual fund. Higher the Units, Higher your shareholding in a Mutual Fund and vice-versa.

Net Assets Value (NAV): A fund's NAV equals the current market value of a fund's holdings minus the fund's liabilities (sometimes referred to as "net assets"). It is computed by dividing net assets by the number of fund shares outstanding. Thus, it's simply the monetary representation of the per unit valuation of the overall fund securities.

Open Ended Funds: Funds with Open Entry and Exit for New and Existing Investors.

Close Ended Funds: These are offered for purchase only once, at the time of their launch. They can further be traded in Stock Exchanges.

Exchange Traded Funds: ETF holds assets such as stocks, commodities, or bonds, and trades close to its net asset value over the course of the trading day. ETFs bear low costs, tax efficiency, and stock-like features.

SIP is an investment vehicle offered by mutual funds to investors, allowing them to invest using small periodically amounts instead of lump sums. The frequency of investment is usually weekly, monthly or quarterly. They are the most popular tools of Investment in Mutual Funds, and allows the investor to Average their purchase cost by periodic investments. They are the best source of Long Term Wealth Creation

Click to QuerySTP is a variant of SIP. It is essentially transferring investment from one asset/ asset type into another asset/ asset type. The transfer happens gradually over a period. Thus, it is Investing ==> from the Invested Fund ==> to Another Fund ==> at periodic intervals.

Click to QueryMutual Funds are subject to Capital Gain Taxes. These gains can be short term or long term. They may be from Equity Oriented Fund or Debt Oriented Fund.

Short Term Captial Gains Tax: 15% for Equity funds sold within 12 months of purchase, and "As per Income Tax Slab" for Debt Funds sold within 36 months of purchase.

Long Term Capital Gains Tax: 0% for Equity Funds sold after 12 months of purchase, and "10% without Indexation" or "20% with Indexation" for Debt Funds sold after 36 months of purchase.

Debt fund has core holdings are fixed income investments with investing objectives as preservation of capital and generation of income. A debt fund may invest in short-term or long-term bonds, securitized products, money market instruments or floating rate debt. They are sensitive to Interest rates of the inherited securities. Longer the Fund's Average Maturity, Higher the volatility. They are good investment options when the interest rates are prone to fall from their ever high.

Click to Query